Swallowing the red herring

Biochar and the elusive economics of field application

Over the last month, I’ve spelled out my hypothesis on why growth in the biochar industry hasn’t lived up to expectations. Over the next few weeks, I’m going to switch gears - focusing on how, and where, we might focus the industry to encourage growth. But first, I want to introduce a frame for that series…

Anchoring and alchemy:

When terra preta was rediscovered in the middle of last century, the alchemy described was captivating. Sand transformed into the world’s most productive soil. I bring this up because I left out something in the last series that feels critical: this captivating story anchored the biochar industry to the assumption that the best use of biochar was as a soil amendment.

However, I think this belief has functioned as a red herring in the development of a meaningful biochar industry. The biochar application par excellence remains terra preta, but for practical purposes it remains unreplicable, unproducible, or at least unaffordable. It is as if we found gold that was the obvious product of an alchemist’s recipe, but then confused knowing that alchemy had taken place with being an alchemist.

If you want to use biochar for field applications, you have two options: either you can make it really cheap or really valuable. Driving down cost implies a lot of investment, which to date, has looked scarce (though there are interesting things happening there). But getting production just right, so the biochar becomes really valuable, is the default goal. But, it’s complicated. To whit, you’re trying to control these input variables:

Feedstock - a natural product and therefore heterogeneous, of varying sizes, with varying moisture content

Process - temperature, duration, type of process

Inoculation - managing (selecting and culturing) the billions of elements of the soil microbiome

Nutrients - natural or chemical? Density and balance of N, P, K? Addition of micronutrients?

Soil - your biochar-based product goes in the ground which is itself exceedingly complex: soil types, existing soil microbiome, drainage etc.

Climate - temperature, precipitation patterns, length of season, microclimates, and on and on.

Plants - how will the crop respond to the biochar you’ve put in the ground? Depends on the plant, of course.

This overwhelming complexity makes testing biochar in the field problematic, and the sales pitch vague. If it worked well, do you know why, and can you predict what will happen next year? Can you determine which variables are determinative, and the ROI? Critically, what can you learn to make your product more valuable?

You can see how iteration and product improvement would be difficult here.

Nevertheless, biochar fairs remarkably well in field tests. It’s often outstanding (especially in degraded soils) - and nearly always performs well enough to encourage many researchers and entrepreneurs to stay on the biochar-as-a-soil-amendment path. Unfortunately, but unsurprisingly, biochar application doesn’t do the same thing everywhere - given the above set of variables, expecting similar results regardless of crop and growing situation would be unreasonable.

There is one more stumbling block: the customer. The focus on biochar as a soil amendment led the community to pick their target market before they could produce the product. Farmers tend to be 1) extremely risk averse because they’re 2) cash poor and often in debt that needs to be repaid this year, and they 3) need huge volumes of soil amendments at 4) shockingly low prices. If you're picking a potential customer for your soil amendment which is expensive, offers usually positive but unpredictable results over very long time lines, is hard to acquire in high volume, and is an unknown quantity to bankers, well, farmers are not a good match.

Thinking this through, it feels obvious why Encendia and so many others struggled to crack this nut. It’s a super hard nut! It’s worth repeating that I think that with advances in our understanding of the soil microbiome, and concurrent improvements in production, field application of biochar will eventually work, and work well. But there are easier, and more profitable, nuts to crack first.

How do we figure out which ones? Good question. To find the answer we need to do a quick interlude:

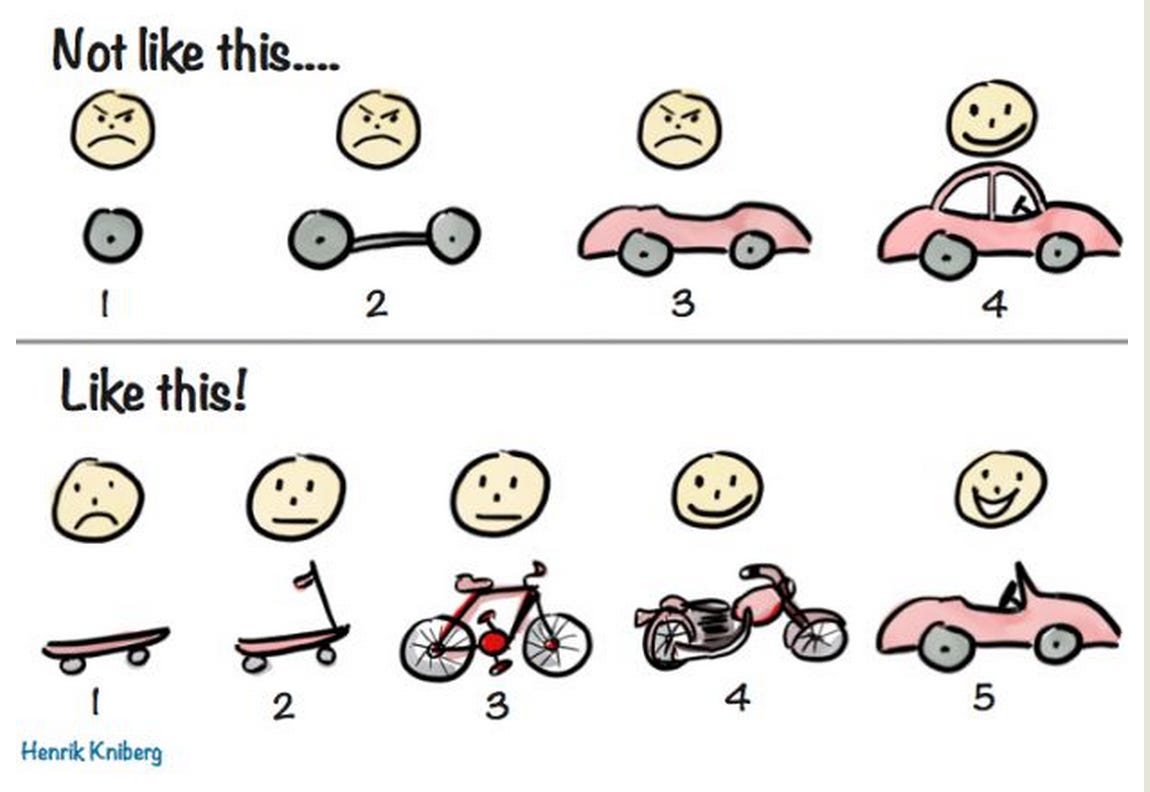

Minimal viable product:

It’s useful to revisit what the tech world calls an MVP (minimal viable product). Below, a classic reminder of what defines a good, and a not so good, MVP.

Do you notice that in the second panel, the product is valuable at each stage, and the value to the customer increases as the product grows? And that the product improvement is clear and predictable? You can even imagine getting valuable feedback at each stage on how to improve the product! Great, right?

Minimum viable industry

MVPs are usually talked about in the context of individual products. However, I think it’s a good mental model for emerging industries and the companies that build them. In order to build something new without first raising massive amounts of money, you often need to focus on high margin products first, and then work your way towards lower margin products as you get better at making things. You’ll see this bear out in any number of markets, but an iconic and recent example is Tesla’s Secret Plan.

In brief: Tesla’s goal was to build a mass-market electric car. But, they started with a sports car that they could put together by hand and sell at high margin, and then increased the speed, volume and sophistication of production. As they grew they were able to drop their per unit cost, and achieve their mission. In their own words: "When someone buys the Tesla Roadster sports car, they are actually helping pay for development of the low cost family car.”

What’s all this got to do with biochar? Well, when you apply this frame to the biochar industry you can see it clearly: nearly all producers are making biochar at relatively low volume, with implied high costs, and extreme product complexity. Instead of focusing on the highest margin applications, they’re focused on the “best” use of biochar: field application, where prices remain low. In the MVP graph above, biochar is stuck somewhere between stage two and stage 3 in the upper panel.

In sum, the biochar industry has tried to skip the low-volume, high margin steps that would allow it to drive down production cost. The predictable result? The target market (farmers) can’t afford the high cost of production, and production can’t scale because of lack of financing and low profitability.

Soil amendment and the goal of terra preta can still be the sector’s north star, but it shouldn’t have been where we started.

So where should we start?

Next week: Sliding down the cost curve

I know, I know, get to the good news! Next week I’ll walk through cost curves and where I think the largest opportunities in the field are, and even some of the levers that could put field application within reach.

Some additional notes:

Check out my most recent interview:

When I’m asked what’s next in biochar, I have a lot of answers. Andre van Zyl, who’s company makes roads with embedded biochar (250 tons of biochar a kilometer!) is at the top of my current list. Check out his interview below.

Highly recommended reading:

I reread Austin Liu’s masterpiece on biochar a couple weeks ago, and it’s just tremendous. If you haven’t read it yet, it’s probably the best single article I’ve found on terra preta. Read it now.

Always good to see this news from the dairy industry!

Open question:

Is anyone doing microwave pyrolysis? Is solar-powered microwave pyrolysis a possibility?

Hey Peter,

thanks for the amazing insights in the economics of the biochar industry! It ended with a cliffhanger about the dilemma of the farmers target goup and it seems like it the further opportunities were never revealed. Does the planned series maybe exists in a raw and unformatted version which never got published? I would love to hear about your thoughts on that topic because it would help us a lot with building our German biochar startup!